MUMBAI (Commoditiescontrol) - Raw and white sugar futures extended the fall on Intercontinental Exchange (ICE) on Friday, over the concern of surplus global supplies.

While raw and white sugar futures also settled 6% down on the week.

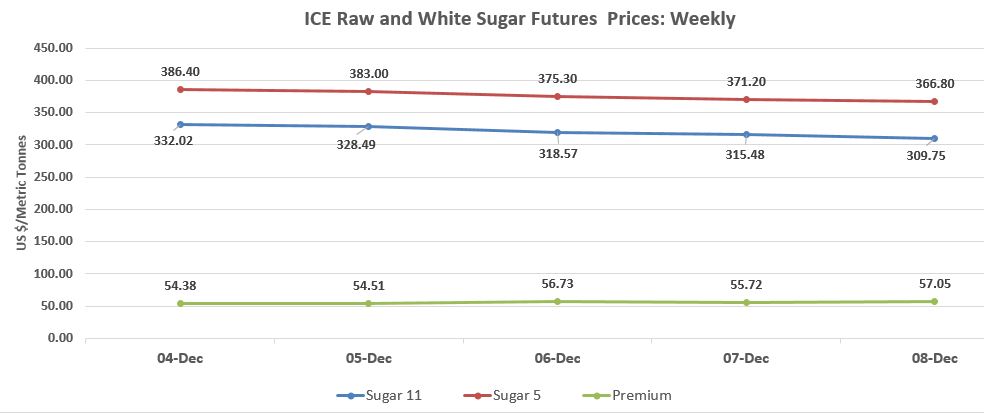

On Friday, ICE March raw sugar closed down 0.26 cents, or 1.82%, at 14.05 cents per pound, after hitting a six week low at 13.97 cents. A lowest level since October 25 for spot price.

While March white sugar futures contract also ended down $4.40, or 1.19%, at $ 366.80 per tonne, after falling at $365.10, a lowest level since October 4.

On other hand, white premium, a whites-over-raws premium remained lower in last week, and traded at $57 per tonne on Friday.

ICE raw sugar futures extended losses from lower closing of last Friday. Raw sugar futures dropped 6.21% in a last trading week, a highest drop since last four months. Sugar futures prices moved down over light speculative buying and stronger dollar. While downfall in the international prices also led the fall in raw sugar futures. And weak technicals also extend the losses of sweetener futures due to selling on technical resistance.

International oil prices also traded down, as price of U.S West Texas Intermediate (WTI) crude oil fell 1.7% and Brent prices also lose 0.5% in a week due to concern of expected rise in production in US. Despite the supply cut by OPEC, Russia and other nine oil producing countries.

While, Petrobras, a state-run oil company of Brazil, also declined the gasoline prices by 2.2% during a trading week. However, low gasoline prices have been consequently lower the demand for the ethanol in Brazil, although sugar mills from Brazil favour the sugar sale over ethanol.

Additionally, the depreciated Brazilian currency against the US dollar also added pressure on raw sugar futures, as this encourages local producers to sell more commodity in international market, and get better returns in real term.

On other hand, London white sugar futures also ruled lower on ICE Europe Exchange, lose 5.68% week on week. Sugar futures continued to fall on estimated excess sugar supply in ongoing season.

White sugar production is expected to increase majorly at the European Union, Thailand, Pakistan, Russia and India.

Accordingly, India, the world's biggest sugar consumer, is expected to produce 24% more sugar in current season, about 245 lakh-255 lakh tonne. While it's neighbouring country, Pakistan will produce nearly 80 lakh tonnes of sugar, a record high sugar output.

Thailand, a second largest sugar exporter of the world, is projected to produce more than 112 lakh tonnes sugar in 2017-18, up 12% from 2016-17. While, Russia, largest beet sugar producer, forecasted to have about 65 lakh tonnes of sweetener output in 2017-18 (Aug-July). Mexico, a another major sugar exporter, is estimated to produce 61.8 lakh tonnes of sweetener, about 3.8% more than the previous season.

Meanwhile, global sugar production is estimated to have surplus sugar output in ongoing sugar season, despite the fall in sugar output at Brazil, due to rise for ethanol demand. Brazil is a world's largest cane sugar producer.

Sugar production of Brazil is estimated at 364 lakh tonne in current season during April 2017 to March 2018 by DATAGRO. While sugar output is expected to fall in next season to 326 lakh tonnes in 2018-19 (Apr-March).

However, the long term trend in global sugar prices are expected to remain weak on surplus production forecasts during 2017-18 and 2018-19 sugar seasons. While strengthening dollar, and weakness in the Brazilian real also keep sweetener futures under pressure.

(By Commoditiescontrol Bureau: +91-22-40015532)