MUMBAI (Commoditiescontrol) - Raw sugar futures ended firm for second consecutive week on Intercontinental Exchange, while white sugar futures finished down, ahead of near month expiry on Friday.

On Friday, ICE October raw sugar settled up 0.28 cents, or 1.96 percent, at 14.55 cents per pound after rising to 14.58 cent, a highest since August 4, while most active March contract also ended up 0.32 cents, or 2.15 percent, at 15.17 cents.

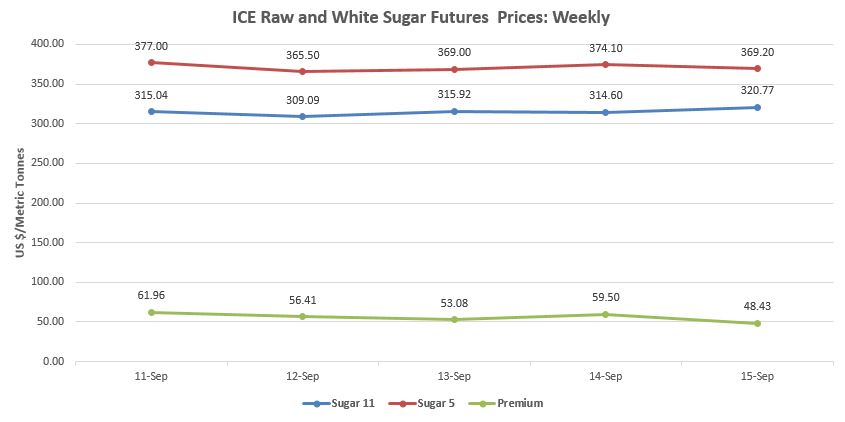

Although October white sugar closed lower $4.90, or 1.31 percent, at $ 369.20 per tonne, on its expiry, while December contract closed up $9.70, or 2.59 percent, at $383.60 per tonne.

On other hand, whites-over-raws premium remained lower in last week, and also touched a lowest level since February 2015.

Raw sugar futures recovered from last session loss, as Brazilian mills favoured ethanol production over sugar. Brazil is the world's largest sugar producer and exporter as well. Brazilian sugar mills and refineries have moved toward ethanol production due to better returns and higher demand. Ethanol demand remained higher in domestic market due to recent hike in taxes, which made ethanol more competitive against the gasoline.

Additionally, federal government of Brazil, also imposed import duty for ethanol import excess than 600 million liters. It also supported the domestic biofuel prices. While recent hike in Brazilian real against the US dollar also helped ethanol pricing.

However, Brazil's center-south region sugar mills have also crushed more amount of sugarcane to produce ethanol instead of sugar in second half of August month and produced 3.15 percent higher ethanol against the last season, according the Brazilian Sugarcane Industry Association (UNICA).

On other hand, white sugar futures were traded weak during last some days, while spot white sugar lost 1.36 percent from previous week. White sugar prices majorly dropped due to the estimated excess sugar supply in global market. As per the initial reports, global sugar supply is estimated to be 2 to 5 million tonnes in 2017-18 (October-September).

The higher sugar supply is expected due to higher sugar production estimate in European Union, a major sugar importer of white sugar. EU is estimated to produce about 20.1 million tonnes of sugar in next season, during October 2017 to September 2018. Highest sugar output since a decade. Sugar production is expected to rise as strict output quotas and export limits will be get abolished from 1st of October 2017. However, sugar imports from EU will be lower in next season, while EU may export sugar in world market, which may increase the exportable sugar quantity in global market.

Additionally, better monsoon rains in Southern Asia, helped cane crop in Thailand, India and Pakistan. Which expected to boost sugar production of the countries. Thailand, a second biggest sugar exporter, expected to produce 11 million tonnes of sugar, while Pakistan, estimated to produce 8 million tonnes of sugar. Although, India, a largest sugar consumer also expected to match countries consumption of 25 million tonnes.

Moreover, white premium also dropped at two and half year low in recent week due to expected higher supplies of white sugar. Although, lower white premium has declined refineries profit margins, due to higher operational costs. But still refineries were buying more raw sugar and increasing their storage due lower rates.

(By Commoditiescontrol Bureau: +91-22-40015532)